All Categories

Featured

Table of Contents

At the end of the day you are purchasing an insurance policy item. We like the defense that insurance coverage uses, which can be acquired much less expensively from an affordable term life insurance policy plan. Overdue fundings from the plan may likewise reduce your survivor benefit, decreasing one more degree of security in the policy.

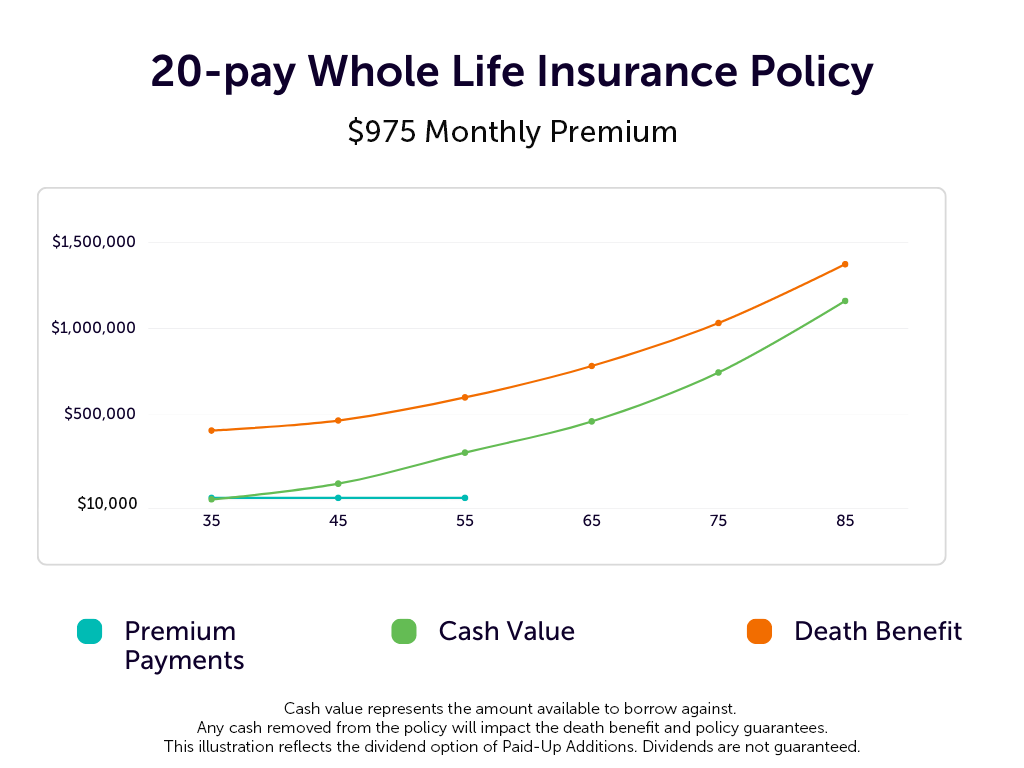

The concept only works when you not only pay the significant premiums, but use extra cash to acquire paid-up enhancements. The opportunity cost of all of those bucks is tremendous incredibly so when you could instead be investing in a Roth Individual Retirement Account, HSA, or 401(k). Also when compared to a taxed financial investment account or even an interest-bearing account, unlimited financial might not offer comparable returns (compared to investing) and comparable liquidity, gain access to, and low/no charge structure (contrasted to a high-yield interest-bearing accounts).

When it involves monetary preparation, entire life insurance policy commonly stands out as a popular option. Nonetheless, there's been an expanding fad of advertising it as a device for "unlimited financial." If you have actually been discovering entire life insurance policy or have come across this concept, you may have been told that it can be a method to "become your very own financial institution." While the idea may seem appealing, it's critical to dig deeper to recognize what this truly suggests and why watching entire life insurance in this means can be deceptive.

The idea of "being your very own financial institution" is appealing due to the fact that it recommends a high level of control over your finances. This control can be imaginary. Insurance coverage companies have the ultimate say in exactly how your plan is taken care of, including the terms of the finances and the rates of return on your cash money value.

If you're thinking about entire life insurance policy, it's necessary to see it in a more comprehensive context. Whole life insurance policy can be an important tool for estate planning, offering a guaranteed survivor benefit to your recipients and possibly using tax obligation benefits. It can also be a forced financial savings vehicle for those that battle to conserve money constantly.

It's a kind of insurance policy with a cost savings component. While it can use consistent, low-risk development of cash worth, the returns are normally lower than what you could accomplish through other investment cars (how to start infinite banking). Before jumping into entire life insurance with the idea of infinite banking in mind, put in the time to consider your economic objectives, threat tolerance, and the complete variety of monetary items available to you

Infinite Banking Concept Pdf

Boundless banking is not a financial remedy. While it can operate in particular circumstances, it's not without threats, and it calls for a substantial dedication and comprehending to manage successfully. By acknowledging the prospective mistakes and understanding the real nature of entire life insurance policy, you'll be better geared up to make an enlightened decision that supports your economic health.

This publication will certainly instruct you exactly how to establish up a financial policy and exactly how to make use of the financial plan to buy real estate.

Limitless financial is not a service or product used by a specific institution. Infinite financial is a method in which you get a life insurance policy that builds up interest-earning money value and get finances against it, "borrowing from on your own" as a source of funding. After that eventually repay the financing and start the cycle all over again.

Pay policy premiums, a part of which develops money worth. Take a funding out against the policy's cash money worth, tax-free. If you use this principle as planned, you're taking money out of your life insurance policy to buy every little thing you would certainly require for the rest of your life.

The are whole life insurance and universal life insurance coverage. The money value is not added to the death advantage.

The plan financing interest rate is 6%. Going this path, the rate of interest he pays goes back into his policy's cash worth rather of a monetary institution.

Be Your Own Banker Nash

The concept of Infinite Financial was created by Nelson Nash in the 1980s. Nash was a money specialist and follower of the Austrian school of business economics, which supports that the worth of items aren't clearly the outcome of conventional economic frameworks like supply and demand. Rather, individuals value money and items differently based upon their economic condition and needs.

Among the challenges of conventional financial, according to Nash, was high-interest rates on loans. Too lots of people, himself consisted of, entered into economic trouble because of dependence on banking institutions. As long as financial institutions established the interest rates and finance terms, individuals didn't have control over their own riches. Becoming your very own lender, Nash established, would certainly put you in control over your monetary future.

Infinite Financial requires you to possess your monetary future. For goal-oriented individuals, it can be the finest economic device ever before. Right here are the advantages of Infinite Financial: Arguably the single most useful element of Infinite Financial is that it enhances your cash money flow.

Dividend-paying whole life insurance policy is extremely low threat and provides you, the policyholder, a lot of control. The control that Infinite Financial uses can best be grouped right into 2 classifications: tax obligation advantages and asset securities. Among the factors whole life insurance policy is excellent for Infinite Financial is exactly how it's taxed.

When you utilize entire life insurance for Infinite Banking, you enter into an exclusive agreement between you and your insurance coverage business. These protections might vary from state to state, they can consist of defense from asset searches and seizures, defense from judgements and protection from lenders.

Whole life insurance policies are non-correlated possessions. This is why they work so well as the economic foundation of Infinite Banking. No matter of what occurs in the marketplace (supply, real estate, or otherwise), your insurance plan keeps its well worth. Way too many individuals are missing out on this important volatility buffer that aids shield and expand wealth, instead splitting their money right into two containers: checking account and investments.

Infinite Banking Reddit

Entire life insurance policy is that 3rd pail. Not just is the rate of return on your entire life insurance coverage policy assured, your fatality benefit and costs are likewise guaranteed.

This structure lines up completely with the principles of the Continuous Riches Technique. Infinite Banking attract those looking for better monetary control. Below are its major advantages: Liquidity and accessibility: Policy fundings offer prompt access to funds without the limitations of typical bank fundings. Tax efficiency: The cash value grows tax-deferred, and plan loans are tax-free, making it a tax-efficient tool for building wide range.

Asset defense: In many states, the cash value of life insurance is protected from lenders, including an additional layer of economic security. While Infinite Financial has its benefits, it isn't a one-size-fits-all service, and it includes significant downsides. Here's why it might not be the very best technique: Infinite Banking usually calls for complex plan structuring, which can perplex policyholders.

Picture never needing to fret about small business loan or high rates of interest again. What happens if you could borrow money on your terms and construct riches at the same time? That's the power of boundless financial life insurance policy. By leveraging the money value of entire life insurance policy IUL policies, you can grow your wide range and borrow money without relying on typical financial institutions.

There's no set lending term, and you have the liberty to pick the settlement routine, which can be as leisurely as paying back the finance at the time of fatality. This versatility includes the maintenance of the lendings, where you can go with interest-only repayments, keeping the lending balance flat and manageable.

Holding money in an IUL taken care of account being credited interest can frequently be much better than holding the cash money on down payment at a bank.: You've constantly desired for opening your own bakery. You can borrow from your IUL plan to cover the initial expenses of leasing a room, purchasing devices, and working with staff.

Dave Ramsey Infinite Banking Concept

Personal car loans can be gotten from traditional financial institutions and cooperative credit union. Below are some crucial points to think about. Charge card can offer an adaptable way to obtain money for very short-term durations. Obtaining cash on a credit rating card is typically extremely expensive with yearly portion rates of interest (APR) commonly getting to 20% to 30% or even more a year.

The tax treatment of policy lendings can vary significantly depending upon your country of residence and the particular terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy car loans are typically tax-free, providing a significant advantage. In various other territories, there may be tax ramifications to think about, such as potential taxes on the financing.

Term life insurance policy just offers a survivor benefit, with no cash value buildup. This indicates there's no cash money worth to obtain versus. This short article is authored by Carlton Crabbe, President of Resources forever, a specialist in supplying indexed global life insurance policy accounts. The details offered in this write-up is for academic and informational objectives just and ought to not be interpreted as monetary or financial investment advice.

For car loan policemans, the comprehensive guidelines enforced by the CFPB can be seen as difficult and restrictive. Initially, lending officers typically suggest that the CFPB's laws produce unnecessary red tape, resulting in even more documents and slower funding processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) guideline and the Ability-to-Repay (ATR) demands, while targeted at safeguarding customers, can bring about delays in shutting offers and raised operational expenses.

{kind=link}

Table of Contents

Latest Posts

Private Banking Concepts

Infinite Banking Concept Reviews

How To Be My Own Bank

More

Latest Posts

Private Banking Concepts

Infinite Banking Concept Reviews

How To Be My Own Bank